Why Money Loses Value Over Time — Inflation Explained in Plain English

Every year, people complain that things are becoming more expensive.

The grocery bill that once cost ₹2,000 now costs ₹2,500. A cup of coffee that cost ₹50 a few years ago costs ₹80 today. Houses, rent, education, healthcare, and even entertainment seem to get more expensive year after year.

Most people notice the price increases.

Far fewer people understand the force behind them.

That force is inflation.

Inflation affects nearly every financial decision you make. It influences your salary, savings, investments, loans, retirement planning, and overall standard of living. Yet despite its importance, inflation remains one of the most misunderstood concepts in economics.

Many people think inflation simply means companies becoming greedy. Others believe governments print money and prices instantly rise. Some assume inflation is always bad, while others think it doesn’t matter unless prices rise dramatically.

The reality is more complex—and more important.

Understanding inflation is essential because it determines whether your money is becoming more valuable or less valuable over time.

This guide explains inflation in simple English: what it is, why it happens, who benefits, who loses, and what you can do to protect your finances.

What Is Inflation?

At its simplest, inflation is the gradual increase in the prices of goods and services over time.

When inflation occurs, each unit of currency buys fewer goods and services than before.

In other words, inflation reduces purchasing power.

Imagine you have ₹100.

Today, ₹100 might buy:

- A movie ticket

- A fast-food meal

- A few household items

Ten years later, that same ₹100 may buy considerably less.

The money itself has not changed.

What changed is its purchasing power.

This is inflation.

When economists say inflation is 5%, they mean that, on average, prices across the economy have increased by about 5% compared to the previous year.

The Hidden Cost of Inflation

One of the reasons inflation is so dangerous is that it often feels invisible.

If someone steals ₹1,000 from your wallet, you notice immediately.

If inflation reduces the value of your money by 5% annually, the effect is much harder to see.

Consider this example.

Suppose you keep ₹10 lakh in cash under your mattress.

If inflation averages 6% per year, the purchasing power of that money declines steadily.

After ten years, your ₹10 lakh may still be ₹10 lakh on paper.

But it will buy significantly fewer goods and services.

You didn’t lose money in terms of numbers.

You lost money in terms of what that money can actually do.

Inflation quietly taxes cash holders without sending them a bill.

Why Does Inflation Happen?

There is no single cause of inflation.

Instead, inflation usually results from a combination of factors.

1. Demand-Pull Inflation

This occurs when demand grows faster than supply.

Imagine a town with 100 houses and 200 buyers.

Since more people want houses than there are houses available, sellers can raise prices.

The same principle applies to:

- Cars

- Electronics

- Food

- Travel

- Services

When demand exceeds supply, prices tend to rise.

This is known as demand-pull inflation.

2. Cost-Push Inflation

Sometimes prices rise because production becomes more expensive.

For example:

- Oil prices increase.

- Transportation costs rise.

- Electricity becomes more expensive.

- Raw materials cost more.

Businesses often pass these additional costs to consumers.

As a result, prices increase throughout the economy.

This is called cost-push inflation.

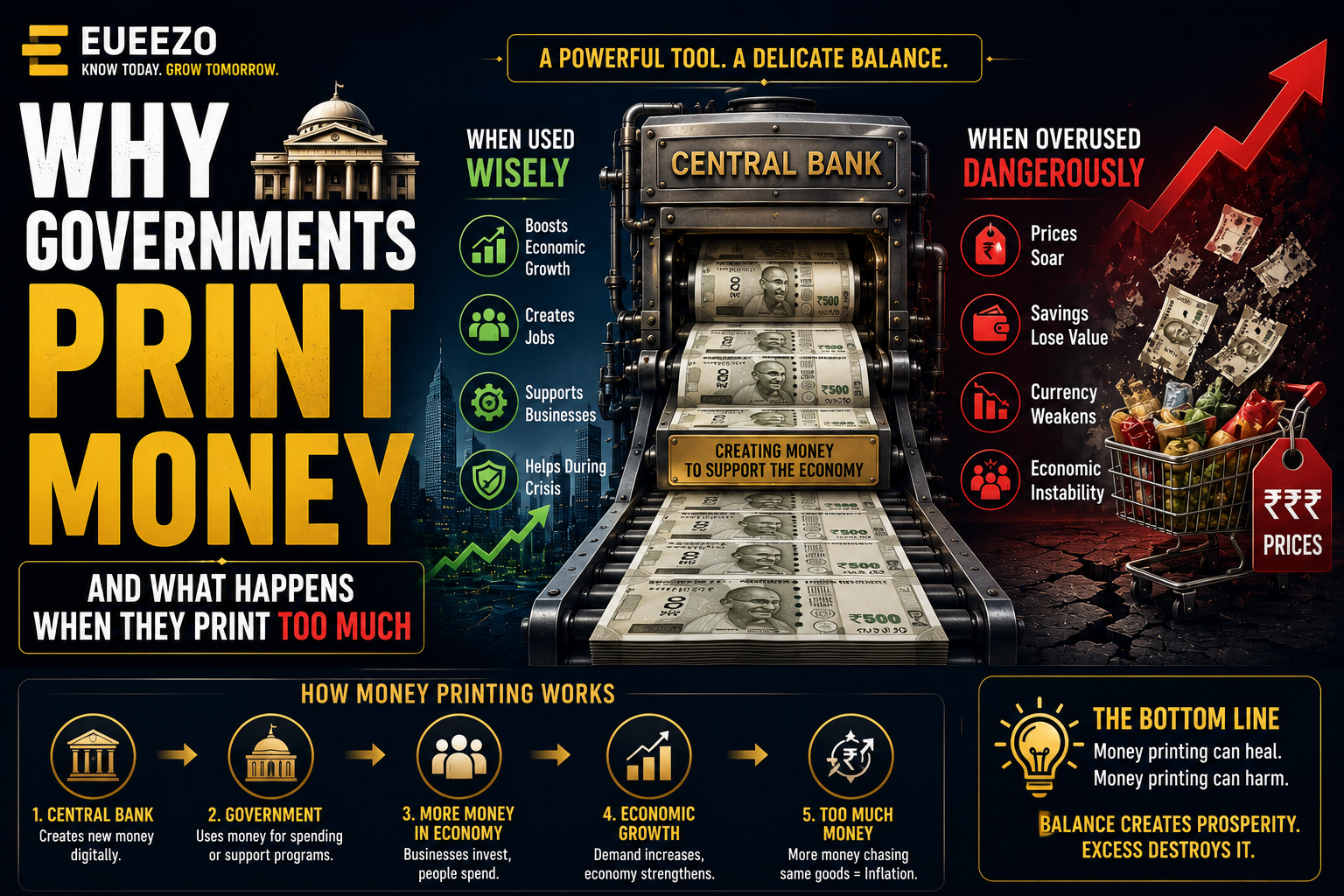

3. Money Supply Expansion

Perhaps the most controversial cause of inflation is the expansion of money supply.

Governments and central banks can create new money through various monetary policies.

When more money enters the economy faster than goods and services are produced, prices often rise.

Think of it this way.

If there are 100 pizzas and ₹1,000 in circulation, each pizza may cost ₹10.

If the money supply doubles to ₹2,000 but there are still only 100 pizzas, prices are likely to rise.

More money is competing for the same amount of goods.

This principle forms the basis of many inflation debates.

Why Central Banks Target Inflation

Many people assume governments want zero inflation.

Surprisingly, they don’t.

Most modern central banks actually aim for low and stable inflation.

For example, many developed economies target around 2%.

Why?

Because moderate inflation can encourage economic activity.

If prices remain stable forever, consumers may delay purchases.

Businesses may delay investments.

Economic growth can slow.

A small amount of inflation encourages spending, investment, and economic activity.

The key word is small.

Moderate inflation can support growth.

High inflation can damage economies.

When Inflation Becomes Dangerous

Not all inflation is equal.

A 2% inflation rate is very different from a 20% inflation rate.

And both are dramatically different from hyperinflation.

Hyperinflation occurs when prices rise extremely rapidly.

Historical examples include:

- Germany in the 1920s

- Zimbabwe

- Venezuela

In extreme cases, people need wheelbarrows full of cash to buy basic necessities.

Savings become worthless.

Businesses struggle to plan.

Economic stability collapses.

Fortunately, hyperinflation is relatively rare.

But even moderate inflation can cause significant damage over time if wages fail to keep pace.

Who Wins During Inflation?

Inflation creates winners and losers.

Let’s start with the winners.

Borrowers

Inflation can benefit people with fixed-rate debt.

Imagine borrowing ₹10 lakh today.

If inflation remains high, future repayments may be made with money that has lower purchasing power.

In simple terms, inflation makes old debt easier to repay.

This is one reason governments with large debts often prefer moderate inflation over deflation.

Owners of Real Assets

Assets such as:

- Real estate

- Businesses

- Productive farmland

- Infrastructure

often increase in value during inflationary periods.

As prices rise throughout the economy, the value of these assets may rise as well.

Companies With Pricing Power

Businesses that can raise prices without losing customers often perform relatively well during inflation.

Strong brands and essential-service providers frequently fall into this category.

Who Loses During Inflation?

Savers Holding Cash

Cash is often the biggest loser.

If your savings account earns 3% interest while inflation is 6%, your purchasing power declines.

You may feel richer because your account balance grows.

But in real terms, you’re becoming poorer.

Fixed-Income Earners

People whose income remains unchanged can struggle during inflation.

If prices rise faster than wages, living standards fall.

Retirees

Retirees relying on fixed pensions may face increasing financial pressure if benefits fail to keep pace with inflation.

This is why many retirement plans incorporate inflation adjustments.

Why Your Salary Needs to Beat Inflation

Many workers celebrate receiving annual raises.

But the important question isn’t:

“Did I get a raise?”

It’s:

“Did my raise exceed inflation?”

Suppose:

- Your salary increases by 5%.

- Inflation is 7%.

Technically, you earn more money.

Practically, your purchasing power decreased.

You can afford less despite earning more.

This concept explains why many people feel financially stressed even when their salaries continue rising.

Real income matters more than nominal income.

Inflation and Investing

One reason investing is so important is inflation.

Cash rarely beats inflation over long periods.

Historically, many investors have turned to assets such as:

- Stocks

- Real estate

- Bonds

- Businesses

- Commodities

to preserve and grow purchasing power.

The goal isn’t simply to make money.

The goal is to increase wealth faster than inflation reduces it.

For example:

If your investments grow 10% annually while inflation averages 4%, your real return is approximately 6%.

This is what actually matters.

Investors focus on real returns, not just nominal returns.

The Relationship Between Inflation and Interest Rates

Inflation and interest rates are closely connected.

When inflation rises too quickly, central banks often increase interest rates.

Higher rates make borrowing more expensive.

This can reduce spending and investment.

As demand cools, inflation may eventually slow.

This is why financial markets pay close attention to central bank decisions.

Interest rates affect:

- Mortgages

- Business loans

- Credit cards

- Savings accounts

- Stock valuations

In many ways, interest rates are one of the primary tools used to manage inflation.

Common Myths About Inflation

Myth 1: Inflation Is Always Bad

Not necessarily.

Low, stable inflation is generally considered healthy for modern economies.

Problems arise when inflation becomes unpredictable or excessively high.

Myth 2: Inflation Only Happens Because Governments Print Money

Money creation can contribute to inflation.

However, supply chain disruptions, labor shortages, energy prices, and consumer demand can also play major roles.

Myth 3: Inflation Affects Everyone Equally

It doesn’t.

Different households spend money differently.

Someone spending heavily on housing and food may experience inflation differently than someone spending heavily on technology or entertainment.

Myth 4: Higher Prices Always Mean Inflation

Sometimes individual prices rise because of specific supply shortages.

True inflation refers to broad price increases across the economy.

How to Protect Yourself From Inflation

You cannot control inflation.

But you can reduce its impact.

Build an Emergency Fund

Emergency savings protect against financial shocks and reduce dependence on expensive debt.

Invest for the Long Term

Historically, productive assets have offered better protection against inflation than holding cash alone.

Increase Your Skills

One of the best inflation hedges is your earning power.

Workers with valuable skills often have greater ability to negotiate higher wages.

Avoid Excessive Cash Holdings

Keeping some cash is essential.

Keeping all your wealth in cash for decades can be costly.

Focus on Real Returns

Always evaluate investments after accounting for inflation.

A 5% return is not impressive if inflation is 6%.

The Future of Inflation

Inflation will likely remain a permanent feature of modern economies.

The exact rate may change.

Some years inflation will be low.

Other years it may spike due to wars, supply disruptions, energy shocks, or economic policy decisions.

But the fundamental principle remains the same:

Money today is usually worth more than the same amount of money tomorrow.

Understanding this simple reality can transform how you think about saving, spending, investing, and building wealth.

The Bottom Line

Inflation is not just an economic statistic discussed by politicians, central bankers, and financial analysts.

It affects your daily life.

It determines how much your savings are worth, whether your salary keeps pace with rising costs, and how effectively you build wealth over time.

The biggest mistake people make is focusing only on how much money they have.

The smarter approach is focusing on what that money can buy.

Because wealth is not measured by the number in your bank account.

It is measured by purchasing power.

And inflation is the force that constantly challenges it.

Understanding inflation won’t eliminate rising prices.

But it will help you make better decisions about saving, investing, earning, and protecting your financial future.