The 50/30/20 Budget Rule: The Simplest Money System That Actually Works

Most people who struggle with money do not struggle because they earn too little.

They struggle because they have no system.

They earn. They spend. They reach the end of the month and wonder where it went. They intend to save but find nothing left to save. They tell themselves they will start budgeting when they earn more — not realising that the problem is not the amount, but the absence of a structure to put it in.

The 50/30/20 rule is the simplest budgeting system that actually works. Not the most sophisticated. Not the most optimised. But the one that requires the least willpower, survives contact with real life, and produces meaningful financial results even for people who hate budgeting.

Here is everything you need to know — what it is, how to apply it to your income right now, where it works and where it doesn’t, and what to do if the math doesn’t add up.

What the 50/30/20 Rule Is

The 50/30/20 rule divides your after-tax income into three categories:

50% — Needs The non-negotiable expenses. Rent or mortgage. Groceries. Utilities. Transportation to work. Health insurance. Minimum debt repayments. These are the things you must pay regardless of everything else.

30% — Wants The things you choose to spend on but don’t strictly need to survive. Restaurants and takeaway. Streaming services. Holidays. New clothes beyond the basics. Entertainment. Gym memberships. These are the expenses that make life enjoyable rather than merely functional.

20% — Savings and Debt Repayment The money you put to work for your future. Emergency fund. Retirement contributions. Investment accounts. Extra debt payments above the minimum. This category is the foundation of long-term financial security.

The framework was popularised by US Senator Elizabeth Warren in her book “All Your Worth” co-authored with her daughter Amelia Warren Tyagi. The core insight was elegantly simple: most financial stress comes not from occasional splurges but from consistently spending too much on the wrong categories — usually needs, which quietly expand to consume everything available.

Why This System Works When Others Don’t

There have been dozens of budgeting systems proposed over the decades. Zero-based budgeting. Envelope budgeting. The cash diet. Pay-yourself-first. Budget apps with sixty-three categories.

Most of them fail in practice. Not because they’re wrong — they’re not — but because they require more cognitive effort than most people are willing to sustain. When a budgeting system requires you to track whether your Tuesday coffee counts as a “morning beverage” expense or an “entertainment” expense, the system is the problem, not your discipline.

The 50/30/20 rule works because it is radically simple. Three categories. Not thirty. Not ten. Three.

This simplicity has specific advantages:

You can calculate it in under a minute. Take your monthly after-tax income. Split it into 50%, 30%, and 20%. You now know your targets. No spreadsheet required.

It has built-in permission to enjoy life. The 30% “wants” category is not a guilty pleasure — it is a structural part of the system. You are not failing your budget when you go to a restaurant. You are using your budget as designed. This psychological shift is significant. Systems that require deprivation are abandoned. Systems that build in enjoyment are maintained.

It is flexible enough for real life. A medical expense does not break the budget — it temporarily shifts from one category to another. A work-from-home month reduces transportation costs and frees up space elsewhere. The broad categories accommodate life’s variability better than granular ones.

It forces the right priorities. The 20% savings allocation is not optional under this system. It is a structural category, not what’s left after you’ve spent everything else. This distinction is everything.

How to Apply It: Step by Step

Step 1: Calculate your after-tax monthly income.

This is your take-home pay — the money that actually arrives in your account after taxes and any mandatory deductions. If your income varies month to month (freelancers, contractors, commission-based workers), use your average income over the past three months and round down to be conservative.

Step 2: Apply the percentages.

| Category | Percentage | Example (£3,000/month) |

|---|---|---|

| Needs | 50% | £1,500 |

| Wants | 30% | £900 |

| Savings & Debt | 20% | £600 |

Step 3: Audit your current spending.

Go through last month’s bank and credit card statements. Categorise every transaction as a Need, a Want, or a Savings contribution. Total each category.

This step is often the most uncomfortable — because most people discover their “needs” have quietly colonised their finances far beyond 50%.

Step 4: Identify the gaps.

Compare your current allocation to the 50/30/20 targets:

- Are your needs above 50%? Something needs to change — either income goes up or a fixed cost comes down.

- Are your wants above 30%? You are lifestyle-inflating faster than your income allows.

- Is savings below 20%? Your future is being funded by your present enjoyment.

Step 5: Make one adjustment at a time.

Do not try to restructure your entire financial life in a week. Identify the single largest gap and address it first. One change sustained is worth more than ten changes abandoned.

What Counts as a Need vs a Want?

This is where most people get tangled. The categories sound obvious until you try to categorise your actual life.

Clear Needs:

- Rent or mortgage payments

- Basic groceries (not restaurant meals)

- Electricity, gas, water

- Internet (in most modern economies — it’s increasingly non-negotiable for work)

- Minimum credit card and loan payments

- Basic transportation to work

- Health insurance

Clear Wants:

- Restaurants, takeaways, coffee shops

- Streaming services (Netflix, Spotify, Disney+)

- Gym membership (unless medically prescribed)

- New clothes beyond replacement of worn-out basics

- Holidays and travel

- Hobbies and entertainment

- Upgrading to a better phone, car, or apartment than the functional minimum

The grey area:

- A car that costs £500/month — need or want? If you need a car to get to work, the car is a need. But a £500/month car when a £200/month car would serve the same function means £300/month has crossed from needs to wants.

- A smartphone — mostly a need in modern professional life. An iPhone 16 Pro Max when an older model would work fine — the premium is a want.

- A gym — probably a want unless you genuinely would not exercise otherwise. But a want you find valuable is still within your 30% to spend on.

The honest question to ask is: “What is the minimum version of this that would meet the actual need?” The difference between what you currently spend and that minimum is a want.

The System in Different Income Situations

The 50/30/20 rule works differently depending on where you are financially. Here is an honest assessment of each scenario:

If you earn a comfortable middle-class income in a developed economy: This system was designed for you. 50% for needs is achievable, 30% for wants gives you a real quality of life, and 20% in savings builds genuine wealth over time. Apply it directly.

If you earn a lower income: The 50% needs allocation may not be enough. Housing alone can consume 40-50% of take-home pay in expensive cities. In this case, the priority shifts: get needs under control first, even if it means savings starts at 10% rather than 20%. A modified 60/20/20 or even 70/20/10 is better than abandoning structure entirely.

If you are in significant debt: Consider a modified version: 50% needs, 20% wants, 30% debt repayment and savings — with aggressive focus on eliminating high-interest debt before building savings beyond an emergency fund.

If you are high-income: The 30% wants allocation can become dangerous at high income levels — £3,000/month on wants is a lifestyle; £15,000/month on wants is a problem. Consider capping the wants category at a fixed number rather than a percentage as income grows.

If your income is irregular: Use the system on a percentage basis rather than a fixed amount. In a strong month, the targets apply as normal. In a weak month, the 20% savings allocation may need to flex — but it should never go to zero.

The 20% Savings Category: How to Actually Use It

The savings and debt repayment category is the most important — and the most misunderstood.

It is not a single bucket. It has a priority order:

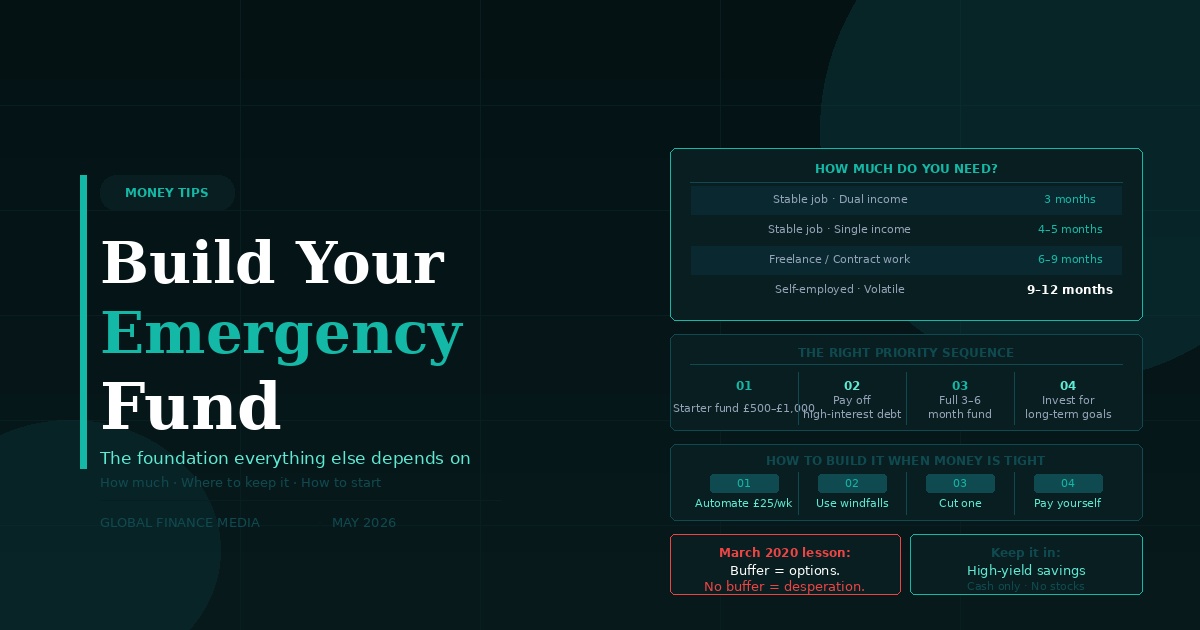

Priority 1: Emergency fund (3-6 months of expenses) Before investing a single pound or dollar, you need a financial safety net. Three to six months of essential living expenses in a liquid, accessible account. This is not a return-generating investment — it is insurance against job loss, medical emergencies, and unexpected expenses. Without it, every financial setback sends you backward.

Priority 2: High-interest debt Any debt with an interest rate above 7-8% should be eliminated before significant investing. Credit card debt at 20% APR is a guaranteed 20% negative return on every pound you leave unpaid. No investment reliably beats that.

Priority 3: Employer pension matching If your employer matches pension contributions, capturing the full match is a 50-100% guaranteed return on that money. This takes priority over additional debt repayment (below high-interest) and non-tax-advantaged investing.

Priority 4: Retirement and investment accounts Once the above priorities are addressed, direct savings into tax-advantaged accounts — ISAs in the UK, 401(k)/IRA in the US, superannuation in Australia, NPS/PPF in India, or equivalent local vehicles. Then index funds and other investments for long-term wealth building.

Priority 5: Other savings goals A house deposit, a major purchase, a sabbatical. Defined goals with defined timelines, funded after the foundational priorities are in place.

The Most Common Mistakes People Make With This System

Treating it as a one-time exercise. The budget audit in Step 3 needs to happen monthly. Not because your categories will change dramatically — but because spending drifts. Subscriptions accumulate. Habits shift. A monthly five-minute review keeps the system calibrated.

Counting gross income instead of net. Always work with take-home pay. Applying 50/30/20 to your gross salary inflates every category and leads to undersaving.

Inflating the needs category. The single most common failure. “I need the expensive apartment” (want). “I need a new car right now” (often a want). “I need this streaming service for my mental health” (want dressed as need). Honest categorisation is harder than the math but more important.

Not automating savings. If savings money sits in your current account until the end of the month, it will not survive. Set up an automatic transfer for your 20% on the day you get paid. Pay your future self before you have a chance to pay your present wants.

Abandoning the system after one bad month. December happens. Weddings happen. Medical bills happen. A month where your percentages are completely off is not a failure of the system — it is a month. Reset and restart.

Does 20% in Savings Actually Build Wealth?

Let’s run the numbers honestly.

If you take home £2,500 per month and save 20% — £500/month — and invest it in a global index fund averaging 7% annual returns:

- After 10 years: approximately £86,000

- After 20 years: approximately £260,000

- After 30 years: approximately £606,000

If you increase your income to £4,000/month and maintain the 20% savings rate — £800/month:

- After 20 years: approximately £416,000

- After 30 years: approximately £970,000

This is not a get-rich-quick promise. It is a slow, reliable, mathematically predictable path to financial security. The 20% savings rate, applied consistently over decades, builds real wealth for ordinary earners without requiring extraordinary income, extraordinary luck, or extraordinary sacrifice.

The people who retire comfortably are not usually the highest earners. They are the people who consistently saved 20% of whatever they earned, for as long as they worked.

Start Today: The Minimum Viable Version

You do not need to perfectly implement 50/30/20 this month. You need to start.

Here is the minimum viable version:

- Calculate your after-tax monthly income right now.

- Multiply by 0.20 — that is your savings target.

- Set up an automatic transfer for that amount on your next payday.

- Spend the rest on needs and wants without guilt — you have already paid your future self.

That is it. One calculation. One bank transfer. One financial habit that, compounded over years, changes everything.

The system does not need to be perfect to work. It needs to be started.

Eueezo breaks down money and business for real people — no jargon, no agenda, no paywalls. Subscribe to our weekly briefing below.